Why premium borrowers get squeezed

The Lemon Problem, famously presented by George A. Akerlof in The Market for “Lemons”: Quality Uncertainty and the Market Mechanism, discusses how asymmetric information leads to an ineffective market.

Now [on to lamens terms], this research shows how both buyers and sellers can arrive at a suboptimal price simply because they do not share the same information.

Here’s why:

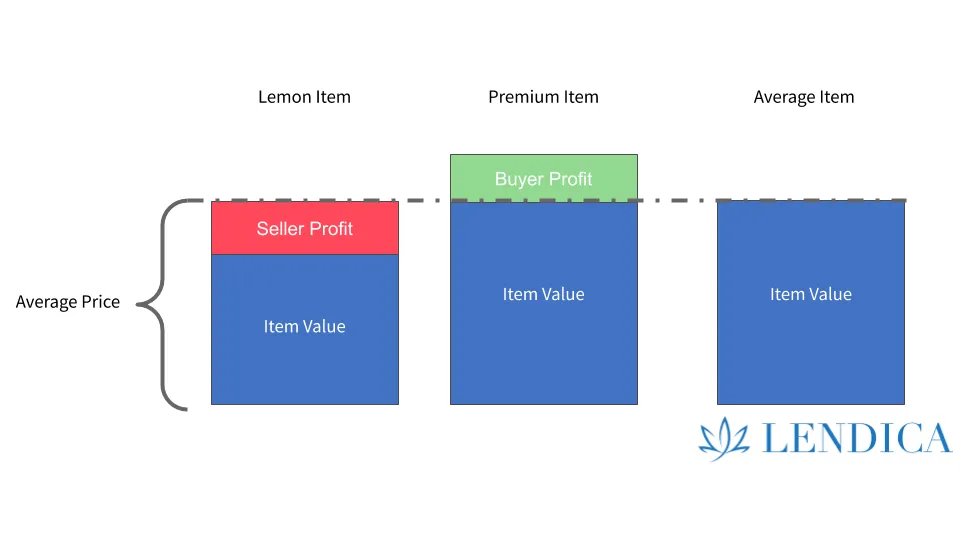

A buyer, knowing they’re out of the know, cannot tell whether their desired item is a premium good or a lemon. Using simple heuristics (fancy way of saying “no clue”), the buyer offers an average price — somewhere between the premium item and lemon item.

When the product is in fact a clunker, the seller wins! The price transacts above the “Item Value” and the difference is their profit. Sadly, and all you quality borrowers best listen up, the seller of the premium item is penalized. The buyer cannot know for certain it’s a premium good and purchases at the average price — below the Item Value (in the chart above, the Item Value is the top of the green box). Again, a profit is pocketed — this time going to the buyer.

On to lending…

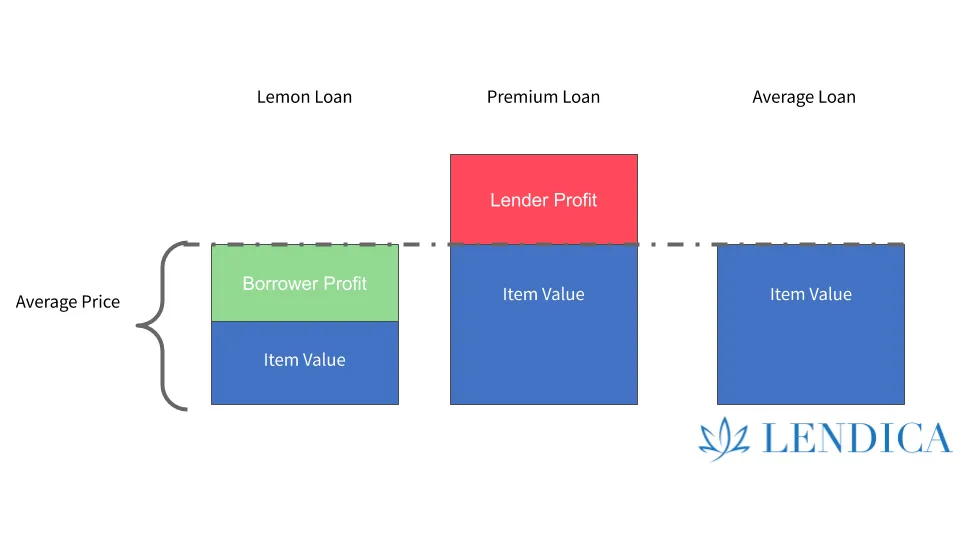

If we replace “Seller” with “Borrower” and “Buyer” with “Lender” we have a similar landscape with slightly different outcomes.

Once again, in almost any case, the Borrower knows more about the business than a Lender. [If not, you may have yourself a lemon :)]. The Lender will not be able to offer the “Item Value,” or true price for your loan, because they do not have enough information to tell Borrowers apart.

What’s worse, the average price is likely not the mid-way point between good and bad. When a loan defaults, the lender can lose up to 100% of its principal. This means they’ll need to make many more good loans to make up for their losses. The result is a much bigger gap between the Item Value and Average Price.

As you can see, the Premium Loan — the quality borrowers running strong operations— are getting poor pricing to make up for the Lemon Loans. The Lender does not have enough information to tell them apart and, like Akerlof’s famous Lemon Problem, are pricing them accordingly. As pleasing as the colors are above, if you are a premium borrower it is not a pretty picture.

Enter Daylit

Daylit has had enough with Akerlof and his lemons.

In today’s information era, there is no excuse for lenders mispricing loans, working capital, factoring or lines of credit. Your business is already teeming with data — POS systems, card processors, inventory tracking, banking, wholesalers, security footage — the list goes on.

So what happens when life gives you data? [Punchline has been removed for obvious reasons]

Daylit helps you take the data that exists throughout your business and add it to your credit profile. We make it simple to export, share, or simply SSO your vendor data into our system. We then use your entire credit picture to offer you the best possible rate.

Remember, it is your data, so make it work for you!

So the next time you get a loan quote and think to yourself, “am I really a lemon,” just remember — only the highest quality borrowers get squeezed. And when you’d like a chilled, refreshing change, come check out Daylit.

{{accelerate-growth-with-working-capital}}